Credit Default Swaps (CDS) became infamous around 2007-2008 and institutions issuing these assets took a notable hit in the ensuing financial crisis. This particular segment of the market has undergone significant changes since its collapse more than 10 years ago. That should be more than enough reason for us to want to examine how it looks today.

Before going further it’s worth quickly reviewing what exactly CDS are. Stocks & Bonds reigned supreme among assets only a few decades ago, however, security markets grew increasingly more complex so banks and other financial institutes had to follow suit to keep up. Today we live in the era of derivatives and CDS fit perfectly into that line-up. In a sense they became the foundation for risk management processes in the 21st century. Simply put CDS allow bond buyers to pass the risks on to the investors who made it their business to take them on in return for a potential profit.

To give an example, a company releases a bond which gets purchased by a bank. The bank then foregoes a part of the returns on the bond in favor of an investor. In return for receiving a share of the interest on the bond, the investor offers to take the risk should the company that originally issued it default. That’s Credit Default Swaps in a nutshell. The bank is allowed to issue it as a separate security because they’re able to accurately evaluate how risky the original bond is. That’s the theory at least.

In practice the CDS market is significantly more complicated than the earlier example suggests. One of the factors that complicates it is that CDS typically don’t contain bonds from only a single company. Instead they contain bonds from a number of different companies with varying levels of risk. It’s also worth pointing out that the entire reason the bank is willing to forego a part of the yields on the bond is because they have concerns about the company that originally issued it. That’s exactly what happened during the subprime mortgage crisis when family homes from Arkansas were bundled together with holiday villas from Florida. The intent was to diversify the risk and make the final product more appealing than the individual mortgages. It also allowed them to hide the risky mortgages behind the safe ones.

Types of Credit Default Swaps

This brings us to the two types of Credit Default Swaps: single-name and multi-name. The former only has bonds from a single debtor and the latter contains bonds from several different debtors packaged into one.

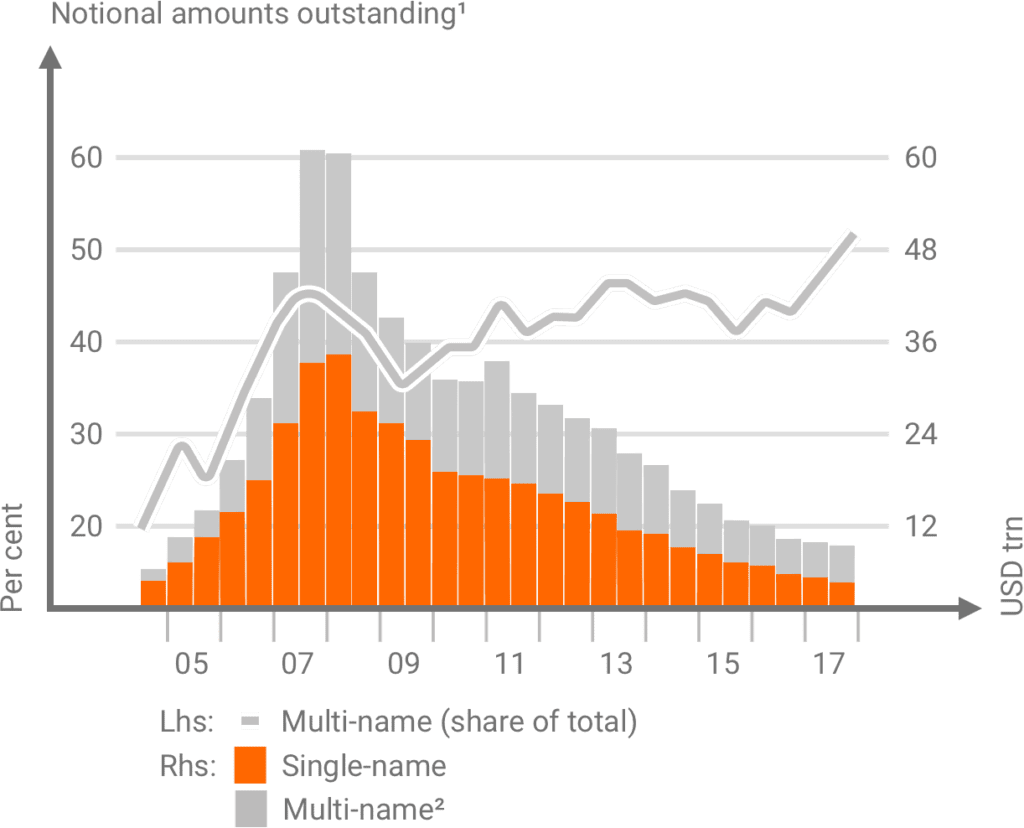

The above chart shows a sudden and sharp increase in CDS releases leading up to their 2007-2008 high. At their peak there was 60 trillion dollars worth of outstanding credit risk on the market. Before 2005 Credit Default Swaps were mainly used to bundle the risk of bonds from either an individual company or bonds from a single country for example. By the time time of the crisis, 45% of them were comprised of multiple debtors. The rate at which total CDS releases rose is almost identical to how quickly the ratio of multi-name swaps increased.

Following the crisis, Credit Default Swaps releases became subject to strict regulation and oversight, which made them significantly less appealing. Over the past 10 years the number of CDS releases steadily declined to the point where in 2018 it was only one sixth of what they were back in 2007. While their numbers today are close to what they were before the crisis, it’s also worth pointing out that the rate of multi-name swaps did not decline. In fact, the opposite happened and today they make up more than 50% of all released CDS. In the end, while they may have fallen out of favor with many investors, they still remain used for the purpose of risk management the same way they came to be used leading up to the crisis.